Insurance covers eating disorders just like substance abuse depression and anxiety

- We are experts at knowing the right codes for the right diagnosis and carrier.

- We have a very good pulse on the national averages of reimbursement and will fight for the correct pricing

- We are experts in the complexities of insurance billing for eating disorders and mental health.

Most policies will cover eating disorders because it falls under behavioral health coverage

- Parity law enforces the coverage of eating disorders.

- We check all benefits before admission to determine eligibility.

- Give peace of mind to your patients of an idea of what to expect $$$ wise.

Axis can speak to families directly regarding eating disorders and their insurance

- We are licensed professionals that actually can advise and enroll patients into the proper health plans.

- We can walk patients through the possibility of reimbursement and set expectations.

- You have direct access through our online software to see where every claim is processing at any given time.

Out of network benefits can help cover the cost 30%-50% of cash pay clients

- Out of network insurance pays above the national average.

- No extra processes on your part, we operate within the business operations you have set up.

- Increase revenue with no extra work.

Do you ask potential admissions if they are using insurance?

- Add insurance reimbursement to your admissions tool belt.

- Know the right questions to ask – (we do that).

- Have confidence in getting claims processed and paid.

How to do ROP and IOP/PHP claims from the facility and/or treating therapist

- We make sure NPI’s are on file and distinguished before submitting claims.

- We make sure you are credentialed as in or out of network depending on your contracts.

- Negotiate with third party pricing companies pre-billing for ease of processing.

Eating Disorder FCode Example for Insurance Billing

- ICD-10-CM Codes

- › F01-F99 Mental, Behavioral and Neurodevelopmental disorders

- › F50-F59 Behavioral syndromes associated with physiological disturbances and physical factors

- › F50- Eating disorders

- › 2021 ICD-10-CM Diagnosis Code F50.9

2021 ICD-10-CM Diagnosis Code F50.9

Eating disorder, unspecified

2020-2021 Billable/Specific Code

- F50.9 is a billable/specific ICD-10-CM code that can be used to indicate a diagnosis for reimbursement purposes.

- The 2021 edition of ICD-10-CM F50.9 became effective on October 1, 2020.

- This is the American ICD-10-CM version of F50.9 – other international versions of ICD-10 F50.9 may differ.

Applicable To

- Atypical anorexia nervosa

- Atypical bulimia nervosa

- Feeding or eating disorder, unspecified

- Other specified feeding disorder

The following code(s) above F50.9 contain annotation back-references that may be applicable to F50.9:

Approximate Synonyms

- Eating disorder

Clinical Information

- A broad group of psychological disorders with abnormal eating behaviors leading to physiological effects from overeating or insufficient food intake.

- A group of disorders characterized by physiological and psychological disturbances in appetite or food intake.

- Eating disorders are serious behavior problems. They include

- anorexia nervosa, in which you become too thin, but you don’t eat enough because you think you are fat

- bulimia nervosa, involving periods of overeating followed by purging, sometimes through self-induced vomiting or using laxatives

- binge-eating, which is out-of-control eating

- women are more likely than men to have eating disorders. They usually start in the teenage years and often occur along with depression, anxiety disorders and substance abuse. Eating disorders can cause heart and kidney problems and even death. Getting help early is important. Treatment involves monitoring, mental health therapy, nutritional counseling and sometimes medicines.

- Group of disorders characterized by physiological and psychological disturbances in eating behavior, appetite or food intake.

ICD-10-CM F50.9 is grouped within Diagnostic Related Group(s) (MS-DRG v38.0):

- 887 Other mental disorder diagnoses

Convert F50.9 to ICD-9-CM

Code annotations containing back-references to F50.9:

- Type 1 Excludes: R13.0

Diagnosis Index entries containing back-references to F50.9:

- Anorexia R63.0

- Aphagia R13.0

- psychogenic F50.9

- Bulimia (nervosa) F50.2

- atypical F50.9

- normal weight F50.9

- Disorder (of) – see also Disease

- eating (adult) (psychogenic) F50.9

- feeding (infant or child) R63.3 – see also Disorder, eating

- or eating disorder F50.9

- specified NEC F50.9

- psychogenic NOS F45.9 – see also condition

- appetite F50.9

Reimbursement claims with a date of service on or after October 1, 2020 require the use of ICD-10-CM codes.

Eating Disorder Billing Codes for Insurance

| Facility/Program Universal Services List | Preferred Codes for UB‐04 Billing | Preferred Codes for CMS 1500 Billing | |||||

| USL # | Standard Services | Revenue Code | Type of Bill Code | CPT/HCPCS Codes | HCPCS Modifier | CPT/ HCPCS Codes | HCPCS Modifier |

| Hospitalization | |||||||

| 1.1 | Hospitalization, Psychiatric | 0114, 0124, 0134, 0144, 0154 | N/A ‐ Bill inpatient services on UB‐04 form | ||||

| 1.2 | Hospitalization, Substance Use Disorders, Rehabilitation Treatment | 0118, 0128, 0138, 0148, 0158 | N/A ‐ Bill inpatient services on UB‐04 form | ||||

| 1.3 | Hospitalization, Substance‐Induced Disorders | 0118, 0128, 0138, 0148, 0158 | N/A ‐ Bill inpatient services on UB‐04 form | ||||

| 1.4 | Hospitalization, Substance Use Disorders, Detoxification | 0116, 0126, 0136, 0146, 0156 | N/A ‐ Bill inpatient services on UB‐04 form | ||||

| 1.5 | Hospitalization, Eating Disorders | 0114, 0124, 0134, 0144, 0154 | N/A ‐ Bill inpatient services on UB‐04 form | ||||

| 1.6 | Hospitalization, 23 Hr Bed, Psychiatric | 0762 | N/A ‐ Bill inpatient services on UB‐04 form | ||||

| 1.7 | Hospitalization, 23 Hr Bed, Substance Use Disorders, Rehabilitation Treatment | 0762 | N/A ‐ Bill inpatient services on UB‐04 form | ||||

| Residential Treatment | |||||||

| 2.1 | Residential Treatment, Psychiatric | 1001 | H0017 or H0018 | H0017 or H0018 | |||

| 2.2 | Residential Treatment, Substance Use Disorders, Rehabilitation Treatment | 1002 | H0011 | H0011 | |||

| 2.3 | Residential Treatment, Eating Disorders | 1001 | H0017 or H0018 | H0017 or H0018 | |||

| Partial Hospitalization | |||||||

| 3.1 | Partial Hospitalization, Psychiatric | 0912 or 0913 | H0035 | H0035 | |||

| 3.2 | Partial Hospitalization, Substance Use Disorders, Rehabilitation Treatment | 0912 or 0913 | H0035 | H0035 | |||

| 3.3 | Partial Hospitalization, Eating Disorders | 0912 or 0913 | H0035 | H0035 | |||

| Intensive Outpatient Treatment | |||||||

| 4.1 | Intensive Outpatient, Psychiatric | 0905 | S9480 | S9480 | |||

| 4.2 | Intensive Outpatient, Substance Use Disorders, Rehabilitation Treatment | 0906 | H0015 | H0015 | |||

| 4.3 | Intensive Outpatient, Eating Disorders | 0905 | S9480 | S9480 | |||

| Facility/Program Universal Services List | Preferred Codes for UB‐04 Billing | Preferred Codes for CMS 1500 Billing | |||||

| Outpatient | |||||||

| 5.1 | Outpatient Therapy Services, Psychiatric/Substance Use Disorders | 0914 0915 0916 | Use appropriate CPTs | Use appropriate CPTs | |||

| 5.2 | Outpatient Aftercare (“Bridge Appointment”) Program | 0513 | |||||

| 5.3 | Applied Behavior Analysis (Autism) | Applicable CPT codes for ABA services | Applicable CPT codes for ABA services | ||||

| 5.4 | Electroconvulsive Therapy (ECT) | 0901 | 90870 | 90870 | |||

| 5.5 | ECT Anesthesia | 0901 | 00104 | 00104 | |||

| 5.6 | Ambulatory, Substance Use Disorders, Detoxification | 0944 or 0945 | H0014 | H0014 | |||

| 5.7 | Ambulatory, Substance Use Disorders, Buprenorphine Maintenance. | 0944 | H0001 H0014 | HG HG | H0001 H0014 | HG HG | |

| 5.8 | Methadone Maintenance | 0944 or 0529 | H0020 | H0020 | |||

| 5.9 | Crisis Stabilization | 0900 or 0914 | S9485 | S9485 | |||

| 5.10 | Emergency Room | 045x | 99281 ‐ 99285 | 99281 ‐ 99285 | |||

| 5.11 | Injections | 96372 | 96372 | ||||

| 5.12 | Home Health Therapy Services | 058x | Applicable CPT codes | Applicable CPT codes | |||

| 5.13 | Nursing Home/Domiciliary or Rest Home Visit | N/A | Applicable CPT codes | Applicable CPT codes | |||

| Ancillary Services | |||||||

| 6.1 | Telehealth Administrative Services | 078x | Q3014 | Q3014 | |||

| 6.2 | Non‐Emergency Transportation | S0209 S0215 A0100 | S0209 S0215 A0100 | ||||

| 6.3 | Emergency Transportation / Ambulance Service | 054x | A0021 A0999 | A0021 A0999 | |||

| 6.4 | Interpreter Services | T1013 | T1013 | ||||

| 6.5 | Laboratory services | 030x | H0003 H0048 | H0003 H0048 |

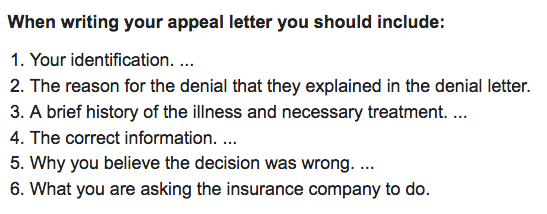

A common occurrence with insurance claims is that they are either fluctuating and underpaying or not paying at all. If someone is not

A common occurrence with insurance claims is that they are either fluctuating and underpaying or not paying at all. If someone is not  Get accredited

Get accredited